Credit score is crucial to US residents. Higher credit scores help you gain trust from lenders to borrow more money. If you are a diaspora starting fresh in the US, you don’t want to miss these tips!

1. Apply for a credit card

It is better to apply to a credit card early to obtain a longer credit history. There are special credit cards that are easier for people with no credit history to get such as “secured” credit cards, store branded cards, and credit-builder cards. These usually have smaller credit limits and higher interest rates. Some may also require a money deposit.

2. Find a co-signer

A co-signer is someone who is willing to take responsibility for a loan or credit card payment if you fail to pay on time. If you have a spouse or close relative with a good credit score, they can cosign for you when you apply for a credit card or loan, which increases the chances your application is approved. If you share finances with someone who already has a credit card, you can also choose to become an authorized user on their account.

3. Report rent and utilities to credit bureaus

There are special reporting services you can use to report your regular on-time payments to credit bureaus to build credit. This works if you are renting and making payments to a landlord. It also works for utility payments. You can ask your water, electric, gas, or cable providers if they report your payments so that they also count towards your score.

4. Pay on time

The best thing you can do to build credit is to pay on-time. It is recommended that you use no more than 30% of your available credit to make sure you can pay it off each month and to avoid paying pricy interest fees.

5. Look out for identity theft

Review your credit card statements and other bills every month so you can detect suspicious activity before it’s too late. Also be careful not to share private information with anyone you don’t trust, especially your Social Security number or ITIN.

6. Monitor your credit report

It is important to monitor credit reports. It is equally important to know and understand how each credit bureau tracks your credit performance. The three major bureaus are Experian, TransUnion and Equifax; and all report your credit differently. There are several credit monitoring services in the market that allows you monitor your credit score.

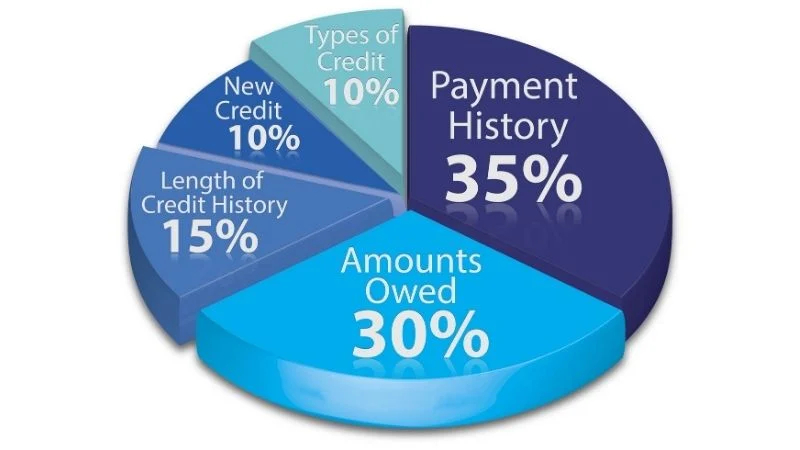

What are the factors that determine your credit score?

1.Payment history

Your payment history accounts for 35% of your score. This shows whether you make payments on time, how often you miss payments, how many days past the due date you pay your bills, and how recently payments have been missed.

2.Amount of debt

Approximately 30% of the score is based on outstanding debt. Your level of debt is predictive of future credit performance because the amount owed typically impacts your ability to pay all monthly credit obligations on time.

3. Length of credit history

Adopt a mindset where you see the length of your credit history as part of your greater long-term credit strategy. Before closing an account, take a moment to consider what impact closing that account may have on your length of credit history.

4. New credit

A new credit card potentially lowers your credit score because an inquiry is placed on your credit report whenever applying for new credit. A new credit card or line of credit will also drag down your average length of credit history and add to your amount of debt.

5. Types of credit

There are three types of credit accounts: revolving, installment and open. It is good to have a mix of different types of credit accounts, though your credit mix likely won’t be the most important factor in determining your scores.